Market Intelligence — Mortgage & Rate Strategy

Jacksonville buyers who saw their rate quote change mid-week are not imagining things. Here is what moved, why it moved, and what to watch next.

Mr. Erin E. King | MBA | CRS | REALTOR | REMLO | Real Estate Strategist | Coldwell Banker Vanguard Realty

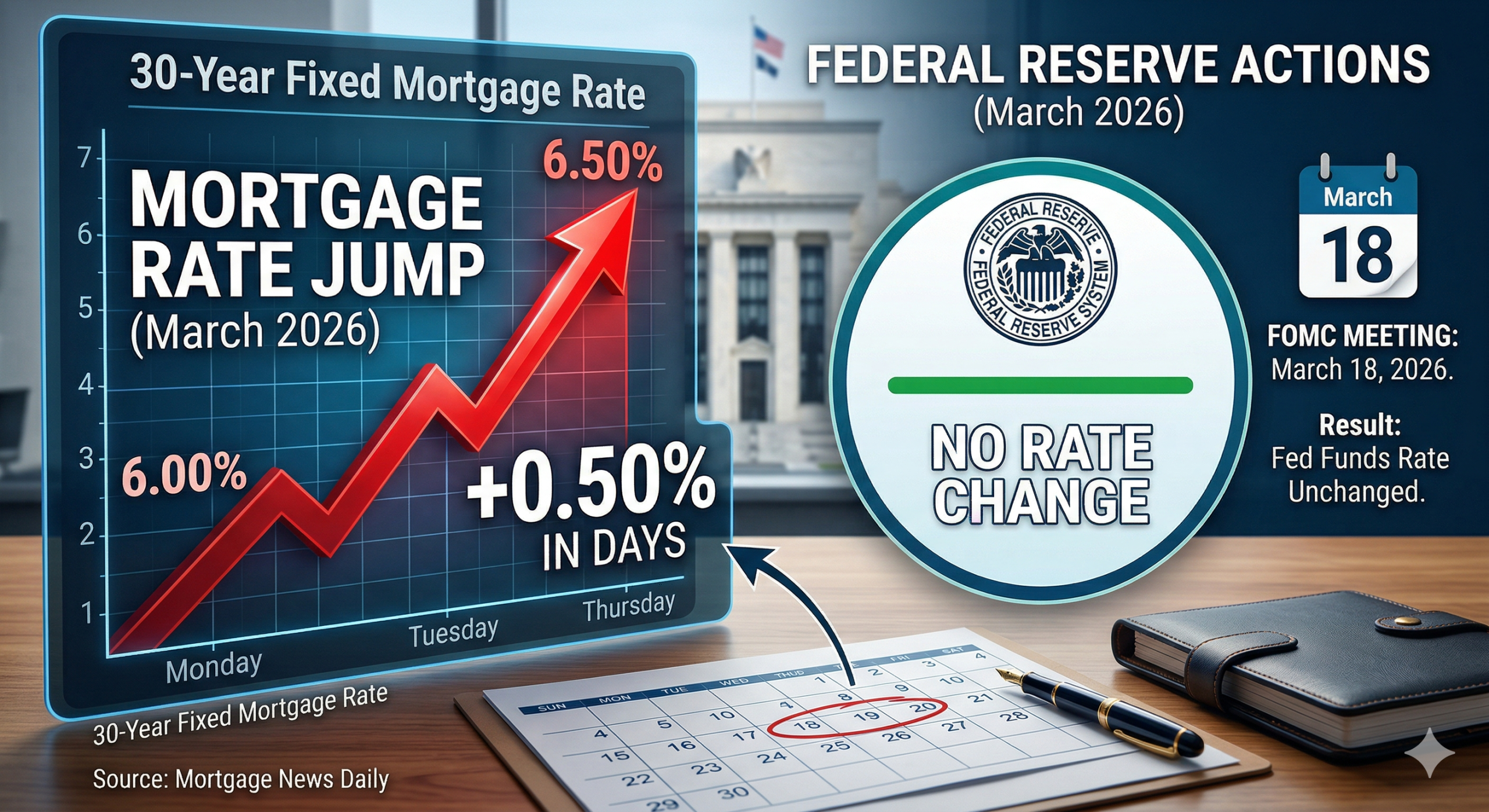

Between Monday and Thursday last week, the top-tier 30-year fixed mortgage rate went from 6.29% to above 6.50%. Three days. Twenty-one basis points. And the Federal Reserve did absolutely nothing. No meeting, no announcement, no policy change. If you called your lender on Monday and got one number, then called back Thursday and got a worse one, you are not imagining things. But you are almost certainly blaming the wrong institution.

30-Year Fixed Rate — Mortgage News Daily (March 17-20, 2026)

6.29%

Monday March 17

6.50%+

Thursday March 20

+21 basis points in 3 trading days — Fed funds rate unchanged

The Bond Market Moved. Your Rate Sheet Followed.

Mortgage rates are not set by the Fed. They are set by investors in the bond market, specifically in mortgage-backed securities, which price off U.S. Treasuries. When Treasury yields rise, MBS pricing weakens, and lenders reprice their rate sheets higher. That is the transmission mechanism, and last week it operated exactly as designed.

What triggered it was a cluster of inflation signals hitting the market in the same week. Oil prices spiked on geopolitical risk. The February Producer Price Index came in hotter than expected, signaling that input costs are still pushing higher. And the March 18 FOMC meeting, while not changing the federal funds rate, was interpreted by traders as more hawkish than the market had priced in. The Fed signaled it is in no hurry to cut. The bond market heard it and repriced accordingly.

Mortgage News Daily, which tracks live lender-facing pricing, showed the 30-year fixed climbing from 6.29% on March 17 to above 6.50% by March 20. The weekly survey from Freddie Mac, which most news outlets cite, lagged the move because it is published on a delay. If you were watching Freddie Mac and thought rates were stable last week, you were looking at last week’s newspaper.

Three catalysts that moved the bond market last week

Oil Price Shock

Geopolitical risk repriced energy costs, pushing inflation expectations higher across the curve.

Hot February PPI

Producer prices came in above expectations, signaling persistent input cost pressure that has not cooled.

Hawkish FOMC Read

The March 18 meeting was interpreted as the Fed signaling no rush to cut rates. Bond traders repriced accordingly.

Why This Was Not a Housing Story

Housing fundamentals were not the driver. Available housing data last week were soft. Existing home sales, inventory levels, pending contracts – none of them screamed “rates need to move higher.” This was a macro inflation shock, transmitted through Treasuries and MBS into the mortgage market. The housing market was a passenger, not the driver.

This distinction matters because it changes what you should be watching. If rates moved because housing was overheating, the fix would come from the housing market cooling. But rates moved because the bond market is worried about inflation. The fix comes from inflation data improving, or from the Fed signaling a more dovish path, or from geopolitical risk receding. None of those are housing variables. You cannot control them by listing your house or sitting on the sidelines.

The bond market does not ask the Fed for permission. It reads the inflation data, interprets the policy signal, and reprices. Your mortgage rate is downstream of that repricing.

What This Means If You Are Buying, Selling, or Refinancing

If you are a buyer under contract, your rate lock matters more than your feelings about where rates are headed. A 21-basis-point move in three days is a reminder that rate locks are insurance, not speculation. Lock when the math works for your payment, not when you think the market has bottomed.

If you are a seller, the rate environment just got slightly less friendly for your buyer pool. Buyers who were pre-approved at 6.3% are now looking at 6.5%, and on a $400,000 loan that is roughly $50 more per month. Not catastrophic, but not nothing. If your home has been sitting, the pricing conversation just got more urgent, not less.

If you are holding a mortgage above 7% and watching for a refinance window, last week was a reminder that the window does not open in a straight line. Rates dropped meaningfully earlier this year and then gave back a chunk of it in one week. Waiting for 5.5% is a strategy. Waiting for perfection is not.

What +21 basis points actually means

~$50/mo

Higher payment on $400K loan

~$18,000

Additional interest over 30 years

3 days

From start to finish

The Real Question Nobody Is Asking

The pattern here is the one I keep coming back to: people blame the Fed for their mortgage rate the same way they blame their thermostat for the weather. The Fed sets the short-term benchmark rate. The bond market sets long-term yields. Your mortgage lives on the long end. Until you understand that distinction, every rate move will feel random and every headline will mislead you.

Last week was not random. It was the bond market doing exactly what bond markets do when inflation data surprises to the upside and the central bank signals patience instead of action. It was mechanical. It was predictable in direction if not in magnitude. And it will happen again.

The question worth sitting with is not “where are rates going next month.” It is whether you understand the machine well enough to make a decision when the next move happens, instead of reacting after it already has. Because the bond market does not wait for you to finish reading the headline.

If you are trying to figure out whether last week’s move changes your math on buying, selling, or refinancing in Jacksonville, reach out directly.

Most people in this situation are getting advice from someone who can only see half the transaction. Schedule a conversation and you get the full picture.

Mr. Erin E. King

MBA | CRS | REALTOR | REMLO

Real Estate Strategist

Coldwell Banker Vanguard Realty

3610 St Johns Ave, Jacksonville, FL 32205

904-999-1780 | Ekingrealtor.com

NMLS: 2809997

Skilled, Diligent, and Trusted. Serving Jacksonville.

{kind=link}

{kind=link}

{kind=link}

{kind=link}