Market Intelligence — Mortgage & Rate Strategy

The Fed Doesn’t Set Your Mortgage Rate

Jacksonville buyers and sellers waiting on a Fed cut are watching the wrong number. Here is what actually moves your mortgage rate, and what to watch instead.

Mr. Erin E. King | MBA | CRS | REALTOR | REMLO | Real Estate Strategist | Coldwell Banker Vanguard Realty

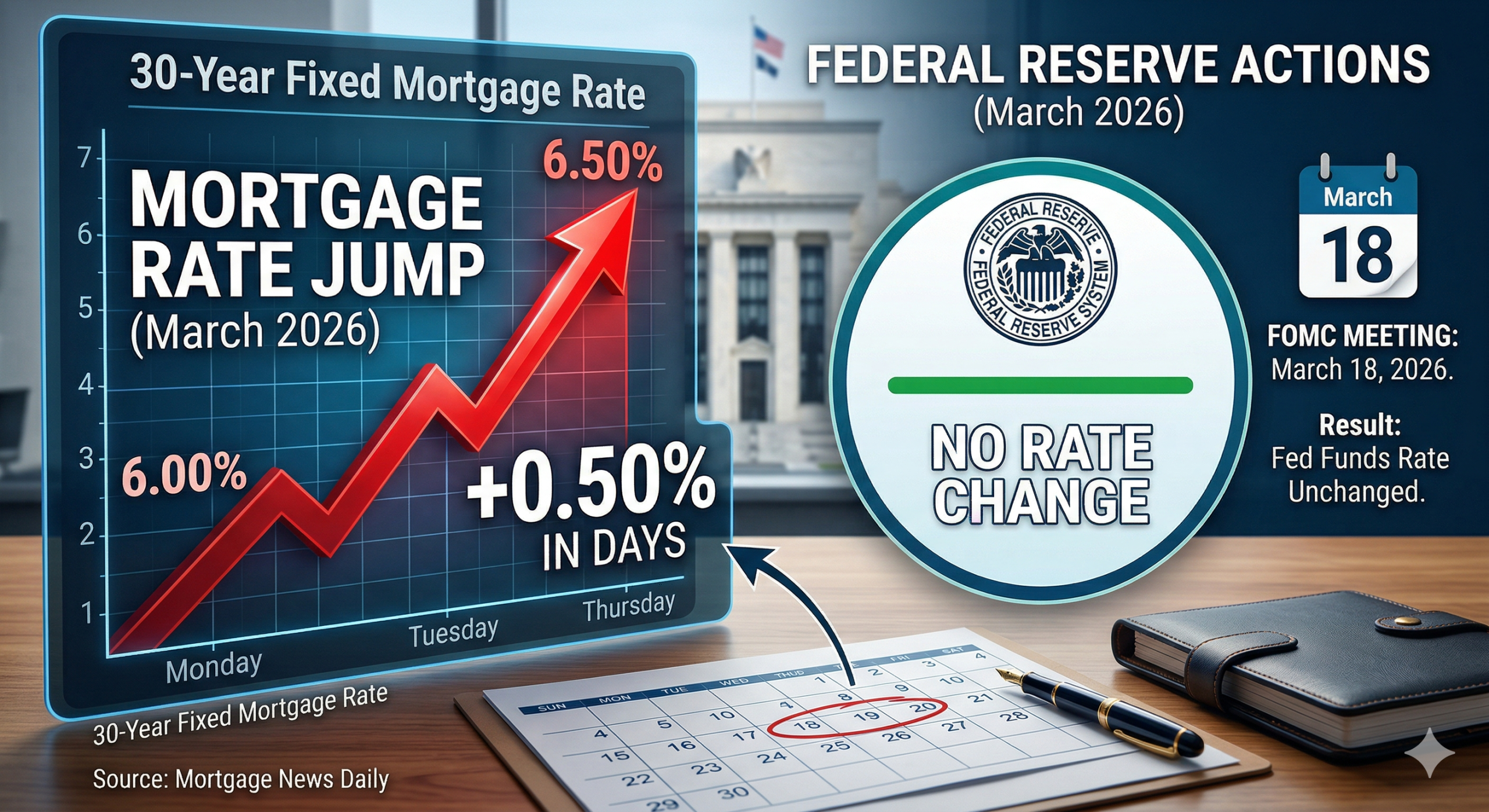

The Federal Reserve cut rates last fall. Mortgage rates went up. If that made no sense to you, you are not confused – you are paying attention. The Fed does not set your mortgage rate. It influences roughly 20% of it. The other 80% answers to a different master entirely, and every buyer and seller in Riverside and Avondale who has been waiting on a Fed signal to make their move is waiting on the wrong thing.

What actually drives your mortgage rate

Federal Funds Rate (Fed controlled) — ~20%

10-Year Treasury Yield & Bond Market — ~80%

The Fed pulls one lever. Bond market sentiment, inflation expectations, and long-term investor demand run the rest of the board. This is why rates can rise the week after a Fed cut.

The Bond Market Is Running the Board

The federal funds rate is the rate banks charge each other for overnight loans. That is it. That is what the Fed controls. What shows up on your Loan Estimate is driven primarily by the 10-year U.S. Treasury yield – a number that moves on bond market sentiment, inflation expectations, and long-term investor demand. Forces the Fed shapes, but does not set.

This is why mortgage rates sometimes rise the week after a Fed cut. Bond investors had already priced in the move, or they read something in the economic data that made them nervous about long-term inflation. The Fed pulled its lever. The bond market went its own direction. Both things happened at the same time, and most headlines are only covering half the story.

The Fed is landing a plane using instruments that give approximate readings. Getting to neutral requires judgment, not just math.

Two Conditions Have to Be True Before Rates Come Down

The Fed is trying to find what economists call the neutral rate – the rate that neither accelerates nor restrains economic activity. The problem is that this number cannot be observed directly. It is estimated through models, and economists disagree on what those models should assume.

Two things have to be true before rates move meaningfully lower.

| 2% Fed inflation target (Core PCE) Currently 2-3%. Closer. Not there. |

2-3% Current Core PCE Early 2026 Trend matters more than any single print. |

1-2 Projected cuts Later 2026 Consensus estimate. Data-dependent. |

Inflation has to come down and stay down. The Fed’s target is 2% annual Core PCE inflation. As of early 2026, that number sits between 2% and 3%. The committee is not looking for one favorable month – it is looking for a sustained pattern across several months before it risks re-igniting what it spent two years fighting. A good January print does not mean February cuts. The Fed watches the trend, not the snapshot.

The job market has to cool without cracking. High employment generally feeds inflation – more people working means more spending, which puts upward pressure on prices. The Fed wants a labor market that softens gradually. A collapsing labor market forces cuts regardless of where inflation stands, and that version of this story is messier and more disruptive for everyone in it.

What to Actually Watch

Current projections from most major financial institutions point toward one or two modest cuts later in 2026. The timing depends on how inflation and employment data develop through spring. These are not exact triggers – they are the directional signals that have historically preceded Fed action.

1

Not one print – a sustained trend. The committee needs to see the pattern hold before it acts.

2

Gradual cooling gives the Fed room to ease. A sharp jump in unemployment changes the calculus entirely.

3

The specific phrasing in FOMC statements and press conferences. When the language changes, the direction is clear.

The Dysfunction Here Is Emotional, Not Economic

The Jacksonville housing market is performing. The problem is not the federal funds rate. Buyers are waiting too long, then acting without the analysis their situation deserves. Sellers are pricing to their aspirations rather than to what comparable sales are actually showing, then spending weeks wondering why showings stopped. Both sides are making decisions based on what they hope is happening rather than what is.

That gap – between hope and reality – is where deals die. It has nothing to do with Jerome Powell.

The buyers and sellers who come out ahead are not the ones who called the rate timing correctly. They are the ones who made decisions anchored to their actual situation: their timeline, their equity position, their household finances, the specific corridor they want to be in. Those variables are knowable right now. The Fed’s next move is not.

What would it take for you to feel confident making a move – buying, selling, or refinancing – regardless of where rates land in the next twelve months? That is the real question. Waiting for certainty from the Fed is waiting for something nobody in this market can give you.

The homeowners who come out ahead are not the ones who predicted the timing. They are the ones who stopped waiting for a permission slip from a central bank that does not set their mortgage rate.

If you want a straight read on what your specific situation looks like in this market – not a forecast, not a pitch – reach out directly.

Most people in this situation are getting advice from someone who can only see half the transaction. Schedule a conversation and you get the full picture.

Mr. Erin E. King

MBA | CRS | REALTOR | REMLO

Real Estate Strategist

Coldwell Banker Vanguard Realty

3610 St Johns Ave, Jacksonville, FL 32205

904-999-1780 | Ekingrealtor.com

NMLS: 2809997

Skilled, Diligent, and Trusted. Serving Jacksonville.

{kind=link}

{kind=link}

{kind=link}

{kind=link}